NEW YORK – Today, MAGNA released their updated US Advertising Forecast.

The updated analysis projects a robust +6.3% increase in advertising revenue, representing the largest increase since 2010.

Key Findings/Top Stories

In its fall forecast update, published October 3, MAGNA Intelligence predicts that media owners net advertising revenues (NAR) will grow by +6.3% to $179 billion this year, the strongest growth rate since 2010 (+6.6%). MAGNA is increasing its full-year forecast from +6.2% in the previous update (June 2016) following a stronger-than expected first-half (up nearly 7% yoy).

In 2017 we anticipate market growth to slow down to +1.4%, mostly due to the lack of cyclical even-year drivers while the underlying demand will remain strong. Neutralizing the record incremental ad sales generated by Political ad spend and Olympic Games (P&O, $3.1bn and 700m resp.) this year, 2016 advertising growth would be +4.4% (similar to last year: +4.3%) and will slow down to +3.5% in 2017.

Digital media advertising sales will grow +15% this year and +12% next year, while traditional media ad sales (consolidating linear television, radio, print and OOH) will decrease by -1.5% this year and -2.2% next year.

Digital advertising sales (all formats) will equal TV ad sales (national and local, including P&Ol) for the first time ever this year, as both will generate approximately $68 billion, i.e. a market share of 38.5%. Digital advertising sales will then reach $105 billion by the end of the decade, a 51% market share.

The main digital media drivers this year are social media (growing +44% this year to nearly $16bn), and online video (+32%). After barely two years of existence, social video advertising already represents $2.2bn (i.e. 14% of total social media NAR or 24% of total video ad formats) and appears to be a massive game changer combining the impact of video and the scale of social media.

Meanwhile National TV NAR remained robust in the first half (+4.6% excl. P&O) thanks to a strong recovery in pricing offsetting the continued decline of ratings supply. For full year 2016 we expect NAR to grow by +3.2% (excluding Olympics), slowing down to +1.5% next year.

In the next four years, MAGNA is predicting holistic video advertising (TV and online video, all platforms, all screens) to grow by a +7% CAGR while holistic audio (radio and audio streaming)will plateau at -1% and holistic print and holistic print NAR (newspapers and magazine, paper and digital) will decline by a – 7% CAGR.

Strong First Half for Advertising Spending

Media owners advertising sales are expected to increase by +6.5% this year (2016) and by +1.5% in 2017. Neutralizing the impact of incremental ad spend driven by even-year events over the period 2015-2017 (“Political & Olympic” effect or “P&O”) advertising sales would increase by +4.4% in 2016 (previously: +4.1%) and by+3.5% in 2017 (prev. +3.4%).

MAGNA is increasing its full-year forecast to +6.3% from +6.2% in the previous update (June 2016) following a stronger-than expected first-half.

Media vendor advertising sales were indeed strong in the first half (+6.1% overall, excl. P&O), arguably over a weak 2015 period. Ad sales were driven by national TV (+4.6%), digital media (+18.3%) and OOH (+3.8%) while print and radio advertising sales continued to decrease (-9% and -2% respectively). The first quarter actually showed the strongest year-over-year growth rate recorded in over a decade (+7.6%, excl. P&O) followed by a robust second quarter (+4.7%). The second half is likely to show weaker growth simply because the 2015 comps will suddenly become much higher leading to a full year growth of +4.4% excl. P&O.

For next year (2017) we anticipate market growth to slow down to +1.4%, mostly due to the lack of cyclical even-year drivers while the underlying demand will remain strong. Neutralizing the record incremental ad sales generated by Political ad spend and Olympic Games (P&O, $3.1bn and 700m resp.) this year, 2016 advertising growth would be +4.4% (similar to last year: +4.3%) and will slow down only slightly to +3.5% in 2017.

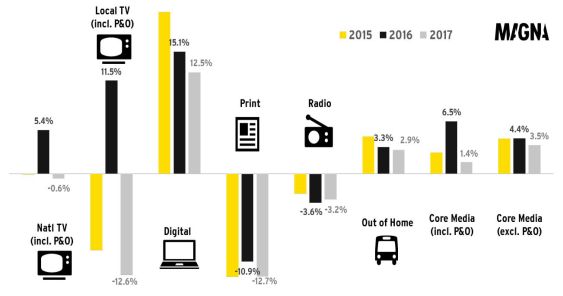

Looking at individual media categories, the +6.3% growth overall for 2016 will be almost entirely driven by digital media (+15% to $68bn) and television (+7.4% to $68bn) while print media and radio advertising sales will continue to decline (newspapers -11% to $12bn, magazines -11% to $8bn, radio -4% to $14bn). Meanwhile OOH media, including cinema, will grow by +4% to $7.5bn. Consolidating all traditional media categories (TV, print, radio, OOH), NAR will decrease by -1.5% this year to $107bn and by another -2.2% next year.

National Television Resilience

National TV NAR grew +4.6%, excluding P&O, in the first half of the year. This compares to a -0.5% decline for the same period in 2015. We expect lower growth in the second half mostly due to stronger comps, but full-year growth should reach a decent +3.2% (excl. P&O).

The growth of advertising revenues for most national television vendors in the last three quarters has been entirely caused by a suddenly more dynamic pricing environment since 3Q15 while, on the other hand, supply continued to shrink (see box).

We believe the sudden re-acceleration of inflation on national television after a couple of years of low inflation(mid-2013 to mid-2015) was caused by supply reaching a tipping point. Many big brands in mainstream advertising verticals, traditionally heavy on national television, have been willing to tolerate higher levels of inflation than before, in order to secure their share of a shrinking supply of traditional linear national television ratings.

Some advertisers in the CPG sector have publicly said that their digital media ad spend had proved disappointing in terms of ROI, which had prompted them to re-allocate more dollars to traditional TV. In fact, advertisers overall did not reduce their digital advertising in the first half, since it grew by an impressive +18%. Advertisers instead grew digital and national TV ad spend, at the expense of print and radio, and thanks to a dynamic national media spend overall.

We believe that the fundamental reason behind the current strength of demand for linear national TV is that large consumer brands in key categories like CPG, personal care or entertainment, still depend on national TV to deliver volume and reach and they don’t perceive digital alternatives to be perfect substitute yet. Part of the issue is likely coming from the fact that cross-screen, cross-platform audience measurement is not universally available yet.

However we believe that those alternatives will gradually become more attractive due to better trading mechanisms, better cross-screen measurement and planning. The deal between MAGNA and Google announced earlier this year was the first-ever TV-style deal between a major agency group and a major digital video provider aimed at making “Google Preferred” Youtube inventory a workable complement or alternative to the shrinking national television inventory, for volume and reach.

Looking at national TV segments, cable networks NAR will grow +3.9% to reach $26bn in ad sales; English-Speaking broadcast networks will grow ad revenues by 8% to $15bn, including an estimated 700 million derived from incremental Olympic sales (excluding Olympics: +2.2%). Spanish-Language networks NAR will grow by 8.5%, in great part due to the incremental sales generated by Copa America, the first-ever Pan-American soccer tournament hosted by the US.

For 2017 we anticipate supply to continue shrinking and pricing to remain dynamic. Total national NAR will grow nevertheless, by +1.5% to $45 billion.

Local Television: No Real Growth Beyond Robust Political Revenues

Local television is facing a similar erosion as national TV in terms of viewing and ratings but it does not experience a similar pricing surge as a result, because of weaker underlying demand. We believe local television stations, and local media more generally, are suffering from the competition of digital media platforms like search and social, whose features (geo-targetability, scalability, accountability, no creative cost, low entry barriers) are increasingly attractive to small and local advertisers. Excluding political ad sales, local TV NAR will down -1% this year to $20 billion.

The good news for local television station is that they remain relevant and dominant over political advertising, far above other traditional local media (print, radio, OOH) and despite the rise of digital political spend (see box). Adding an estimated $3 billion in incremental political ad sales this year, total local TV sales should grow by +12%.

Social Video: A Game Changer

Digital media NAR are forecast to grow by 15% this year to reach $68 billion. Growth is entirely driven by mobile-based impressions (+45%) while desktop-based impression generate stagnating ad sales (-0.6%). In terms of formats, video and social continue to show explosive growth (+32% and +44% respectively) while search will grow by a robust 14%. Meanwhile, static display banners will start to attract fewer dollars due to lower demand and ad blocking.

As predicted by MAGNA for the last two years, 2016 is the year when digital media ad sales finally equal television ad sales making digital media the #1 category, as the curves cross each other at $68.5bn or 38% market share. From that point, digital media will grow to $105 billion by 2020, a 51% market share.

Video formats and social media have been growing faster than other digital media environments or formats in the last few years, but the irruption of social video in the last eighteen months has brought this to yet another level. Between 2014 and 2016 social media ad sales have more than doubled, from $7bn to $16bn and so did digital video ad sales (from $4bn to $9.5bn)but while those were neatly divided back in 2014, we now have a quickly growing overlap: social video. MAGNA estimates that social video ad sales will reach $2.2bn this year, which already represents 14% of total social media sales and 24% of total video formats ad sales.

Among the factors that are fuelling the rapid growth of social video is the interest of big brands that were previously spending very little on social networks and are now willing to take advantage of the huge scale and reach provided by social networks. Despite the recent glitch in Facebook viewing metrics, we believe the appeal of video advertising within social networks (not only auto-play commercials in newsfeeds but also, potentially, live event streaming as experienced by Twitter and the NFL) is here to stay. It will partly cannibalize existing digital video platforms (Youtube, Hulu, Full Episode Players and long tail video networks) but it will mostly grow both the digital video pie and the social media pie.

Putting together traditional linear television ad sales, traditional forms of digital video and the newly emerging social video segment, we find that holistic video ad market will grow to 100 billion by 2020, of which a third, $33 billion will be derived from the various forms of digital video.

Meanwhile programmatic technologies continue to reshape digital media trading. This year, the programmatic and automated transactions for display and video ad impressions will reach $10 billion i.e. approximately 35% of total display/video ad sales.

Towards “Holistic” Media Categories

The traditional way of breaking down advertising sales by media category (TV, print, radio etc.) becomes increasingly irrelevant as media owners originally centered in those formats now deliver their content and ad loads over digital platforms and devices too. For that reason MAGNA will now systematically provide additional estimates and forecasts broken down in “holistic” media genres: video (TV plus digital video), audio (radio plus digital audio) and print (paper-based ad sales plus digital sales).

Looking at the cross-platform ad sales that traditional media owners are generating through digital platforms enables us to mitigate what might otherwise feel like dramatic, irreversible declines. Looking at the long-term NAR dynamic for “audio” for instance, we find that while “legacy” ad revenues (broadcast linear radio) will decline by -4% CAGR over 2016-2020, digital audio ad sales will grow by 13% and the total genre will only decline by -1% per year over the period. In the print sector too, the rise of digital advertising revenues will not quite offset the erosion of ad sales on “legacy” formats: legacy CAGR of -16% and a digital CAGR of 11% will lead to a consolidated CAGR of -7% over 2016-2020. Finally for “video”, we foresee legacy NAR to stagnate over 2016-2020 while digital video (including social video) will grow +39% per year and the combine video market will grow by +7% over the period.

—————-

The next US Advertising Revenue Forecasts by MAGNA will be published in December 2016.

—————-

Beyond the present report, MAGNA employees and subscribers interested in the fall update of our US Ad Forecasts can also use our powerpoint deck and our detailed excel file, available on atlas.magnaglobal.com.