GLOBAL – The latest Media Economy Report from MAGNA Intelligence, focuses on Out-of-Home (OOH) Advertising trends globally. A joint study in partnership with IPG Mediabrands’ out-of-home specialist agency, Rapport, the report, entitled Why Out-of-Home Outperforms, is based on an analysis of the global OOH industry and OOH advertising in 70 countries.

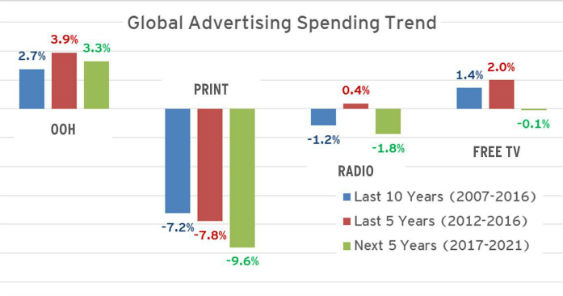

According to MAGNA, OOH advertising is now a $29 billion market, responsible for approximately 6% of the $500 billion global advertising spending. However, OOH market share increases to 10% to 12% in some countries, including France and Russia, compared with other media categories including Internet, TV, print and radio. OOH market share has remained stable in the last five years, hovering around 6%. However, as part of its increasing importance in the media mix, OOH market share has increased from 8% to 10% of traditional media advertising spend, which includes TV, print, radio and out-of-home, among other categories.

MAGNA Intelligence, in partnership with Rapport, conducted an in-depth survey in 22 key markets including Argentina, Australia, Belgium, Canada, China, Denmark, France, Germany, India, Italy, Japan, Malaysia, Mexico, Netherlands, Norway, Philippines, Russia, Singapore, Spain, Thailand, United Kingdom and the United States. The objective of the survey was to assess OOH advertising’s sustained growth and impact during a period where offline marketing budgets are stagnating and other media categories are struggling.

Below are 10 key reasons behind the resilient and consistent performance of OOH media in those markets.

- Everybody is outside! OOH remains a mass reach medium, reaching at least half of consumers in most markets and as much as 90% in some. Out-of-home stands alongside TV and radio as a way to communicate at scale. In the majority of markets assessed, OOH reach and audience are mostly immune from the erosion and fragmentation experienced by television or print.

- OOH audience measurement continues to improve. With technological advancements in areas such as electronic location data and eye-tracking, markets including the U.S., U.K., and Germany are leading the charge on more sophisticated out-of-home measurement. The U.S. market is at the forefront of innovation in OOH media measurement with the recent launch of MORE by Geopath. Thanks to various technologies including Eye-Tracking, OOH measurement gradually gets closer to measuring actual impressions (“Likelihood-to-See”) rather than just “opportunities to see” (traffic within viewing distance of an ad unit).

- OOH advertising cannot be skipped or blocked. Media consumers, and generation X and Y especially, have become experts at avoiding advertising by choosing ad-free, paid-for media or blocking ad insertions on free websites. OOH is largely immune from that threat.

- Digital OOH is boosting advertising revenues by creating more opportunities for marketers in premium locations like airports or malls, thus increasing the revenue per panel multiple times. Although digital units account for only 5% of the global OOH inventory, they already generate 14% of total advertising revenues. In fact, DOOH already accounts for 30% of revenues in some markets like the UK and Australia, and the global share is predicted to grow to 24% globally by 2021.

- OOH inventory becomes more impactful and valuable. According to the MAGNA and Rapport study, the total volume of OOH advertising units is not expanding globally. In many markets, it is actually shrinking, as large-format static billboards are being gradually dismantled or replaced by fewer, more high-quality back-lit rolling panels or digital panels. The OOH industry is engaged in a process that feels necessary but complicated for other media categories (TV, radio, print): cutting clutter to increase the impact value of inventory.

- Transit and Street Furniture are still developing. In many markets, regulation and public governance have reached a point where transportation authorities and municipalities are ready to partner with OOH vendors to generate advertising revenues. These OOH segments are typically based on long-term contracts (10 to 15 years) and the renewal/RFPs being negotiated now are often the first to come up in the context of affordable digital screens, connectivity and programmatic opportunities. This is why digital inventory has increased by approximately 30% over the last two years. For instance, the renewal of the Street Furniture contract in Madrid and Barcelona, or the New York bus shelters in 2016, all led to a jump in digital inventory and revenues. Big contract renewals in 2017 include New York’s Metropolitan Transport Authority, where the authority is looking to aggressively develop digital opportunities.

- OOH is expanding to brand new environments. Digital screens have allowed OOH advertising vendors to penetration niche environment allowing to reach young urban population that is otherwise hard to reach by traditional media: offices, elevators, taxi, gyms, bars, retail etc. The “Digital Place-Based” segment offers targeting capabilities and programmatic opportunities.

- OOH becomes addressable and experiments with programmatic. Programmatic technologies initially developed to automate the trading of online display ads, are now being used in to buy and optimize ad campaigns on connected DOOH units.

Programmatic techniques not only optimize the workflow of media-buying but help brands deliver the right ad in the right place and at the right time, using consumer data and mobile location data. Giving advertisers the ability to plan, buy, optimize and measure the effectiveness of their outdoor campaigns through an online platform represents the natural evolution of OOH’s technology-driven transformation with many vendors developing Private Marketplaces (PMP).

OOH can address branding campaigns as well as lower funnel activation.

Positioned in transportation and shopping malls, OOH has an inherent ability to target consumers at or near point-of-sale. Now connected digital screens, usage of smartphone data and marketing data allow marketers to target specific day parts, target groups and location with increasing relevance.

10. OH can go native. “Native” is the buzzword for ad campaigns to become more acceptable and impactful by avoiding standardized formats and merging in the editorial context. OOH has a long history of creatively playing with formats and environments; moving image and connectivity bring that to a new level today. Specialized operations, which rely on customized equipment, interactivity, unexpected location, have the capacity to surprise, entertain and engage consumers. Finally OOH can go real time: Digital connection also means that OOH campaigns can occasionally reflect live events (sports results, lottery draws, weather, traffic etc.)

Mike Cooper, Global CEO of Rapport said: “With the explosive growth of digital-out-of-home (DOOH), the diversified lifestyle touch points it reaches, and the veritable mountain of mobile driven audience data, we are best positioned to accurately, and in real-time, track audiences and deliver contextually relevant messages through out-of-home media. OOH’s sustained growth on a global scale will further enable us to create engaging consumer experiences.”

Vincent Létang, EVP, Global Market Intelligence at MAGNA said: “Thanks to favorable lifestyle evolutions, innovation and investment from media owners and public authorities, OOH has been the only ‘traditional’ media category to show consistent growth in the last ten years, while TV and radio have stagnated and print sales have declined. MAGNA predicts this will continue: OOH advertising revenue will grow by 3% to 4% per year in the next five years to reach $33 billion by 2021.